import numpy as np

import scipy as sp

import matplotlib.pyplot as plt

plt.style.use("fivethirtyeight")We have seen the Metropolis algorithm in previous example, now we address the Metropolis-Hastings Algorithm which is a more general form of the former one.

The different between a Metropolis and a Metropolis-Hastings (MH) algorithm resides on acceptance rule, MH has a correction factor \[ P_{\text {accept }}=\min \left(\frac{P\left(\lambda_{p} \mid y\right)g(\lambda_{c}|\lambda_{p})}{P\left(\lambda_{c} \mid y\right)g(\lambda_{p}|\lambda_{c})}, 1\right) \]

where subscripts are simplified as \(c\) and \(p\) which represent current and proposed accordingly. The correction factor is \[ \frac{g(\lambda_{c}|\lambda_{p})}{g(\lambda_{p}|\lambda_{c})} \]

The Metropolis–Hastings correction factor is the probability density of drawing the current value (\(\lambda_c\)) from a distribution that is centered on the proposed value (\(\lambda_p\)) divided by the probability density of drawing the proposed value (\(\lambda_p\)) from a distribution centered on the current value (\(\lambda_c\)).

The intention of correction factor, as its name indicates, is to correct the asymmetry of proposed distribution. We have only used normal distribution so far, which automatically has \(\frac{g(\lambda_{c}|\lambda_{p})}{g(\lambda_{p}|\lambda_{c})}=1\).

In this section, we can demonstrate how an asymmetrical proposed distribution works and how we can correct the asymmetry.

Revisit Beta-Binomial Conjugates

We will turn to a Beta-Binomial conjugate example to demonstrate HM algorithm and especially the mechanism of correction factor. To reproduce the example here.

Suppose we would to like to how estimate a basketball player’s free throw probability. For the prior, since we don’t know much about him, he can be either an excellent or an awful player, so we choose \(\alpha_0=\beta_0=.5\), the subscript zero represent priors. The plot tells our subjective view toward the player, he either has very high or very low probability of scoring.

x = np.linspace(0, 1, 100)

params = [0.5, 0.5]

beta_pdf = sp.stats.beta.pdf(x, params[0], params[1])

fig, ax = plt.subplots(figsize=(7, 7))

ax.plot(

x, beta_pdf, lw=3, label=r"$\alpha = %.1f, \beta = %.1f$" % (params[0], params[1])

)

ax.legend()

ax.axis([0, 1, 0, 3])

plt.show()

The likelihood is binomial and posterior is again a beta distribution. However, in MH algorithm we need to specify one more distribution which is proposed distribution.

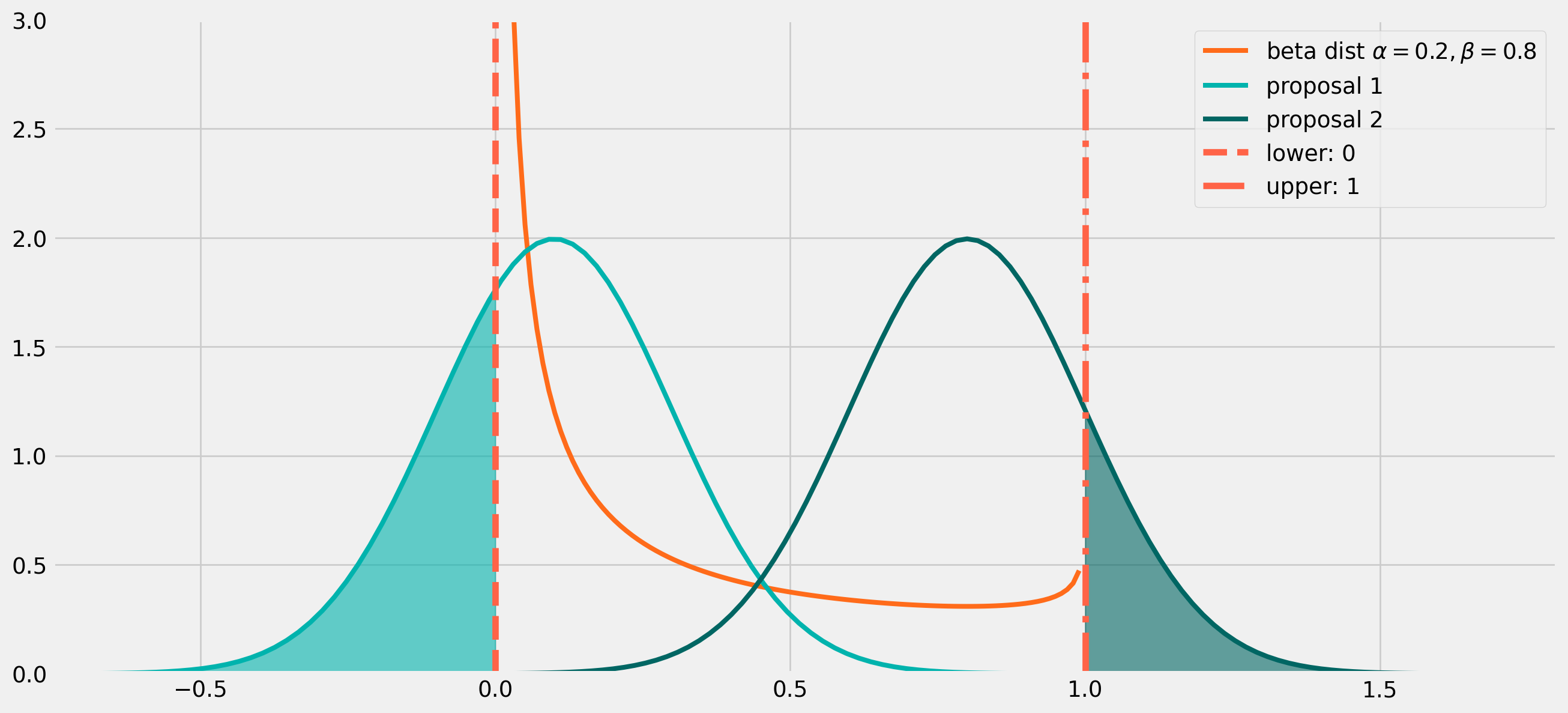

Can we use a normal distribution as proposed distribution here? Well, technically you can, but it’s not the ideal distribution.

The problem is easy to see from the plot below.

If the proposal distribution is centered close to \(0\), the draw could easily return a negative number, as the light green shaded area on the left shows, which could be remedied by multiply \(-1\). However if the proposal distribution is centered close to \(1\) as shown in the darker green area on the right, the draw could be larger than \(1\). It’s attempted to correct these outliers by minus \(1\), however there is no easy remedies for this issue, since the random draw can be \(2\), \(3\) or even larger numbers.

x_beta = np.linspace(0, 1, 100)

x_norm_1 = np.linspace(-1, 1, 100)

x_norm_2 = np.linspace(0, 1.8, 100)

params_beta = [0.2, 0.8]

beta_pdf = sp.stats.beta.pdf(x_beta, params_beta[0], params_beta[1])

mu_1 = 0.1

sigma_1 = 0.2

norm_pdf_1 = sp.stats.norm.pdf(x_norm_1, loc=mu_1, scale=sigma_1)

mu_2 = 0.8

sigma_2 = 0.2

norm_pdf_2 = sp.stats.norm.pdf(x_norm_2, loc=mu_2, scale=sigma_2)

fig, ax = plt.subplots(figsize=(15, 7))

ax.plot(

x_beta,

beta_pdf,

lw=3,

label=r"beta dist $\alpha = %.1f, \beta = %.1f$"

% (params_beta[0], params_beta[1]),

color="#FF6B1A",

)

ax.plot(x_norm_1, norm_pdf_1, lw=3, label=r"proposal 1", color="#00B3AD")

ax.plot(x_norm_2, norm_pdf_2, lw=3, label=r"proposal 2", color="#006663")

x_fill = np.linspace(-1, 0, 30)

y_fill = sp.stats.norm.pdf(x_fill, loc=mu_1, scale=sigma_1)

ax.fill_between(x_fill, y_fill, color="#00B3AD", alpha=0.6)

x_fill = np.linspace(1, 1.8, 30)

y_fill = sp.stats.norm.pdf(x_fill, loc=mu_2, scale=sigma_2)

ax.fill_between(x_fill, y_fill, color="#006663", alpha=0.6)

ax.axvline(0, color="tomato", ls="--", label="lower: {}".format(0))

ax.axvline(1, color="tomato", ls="-.", label="upper: {}".format(1))

ax.legend()

ax.axis([-0.75, 1.8, 0, 3])

plt.show()

Therefore the best proposal distribution is bounded within \((0,\ 1)\), which is exactly a beta distribution does.

To summarize, our prior and posterior are beta distributions, so is proposal distribution of posterior!

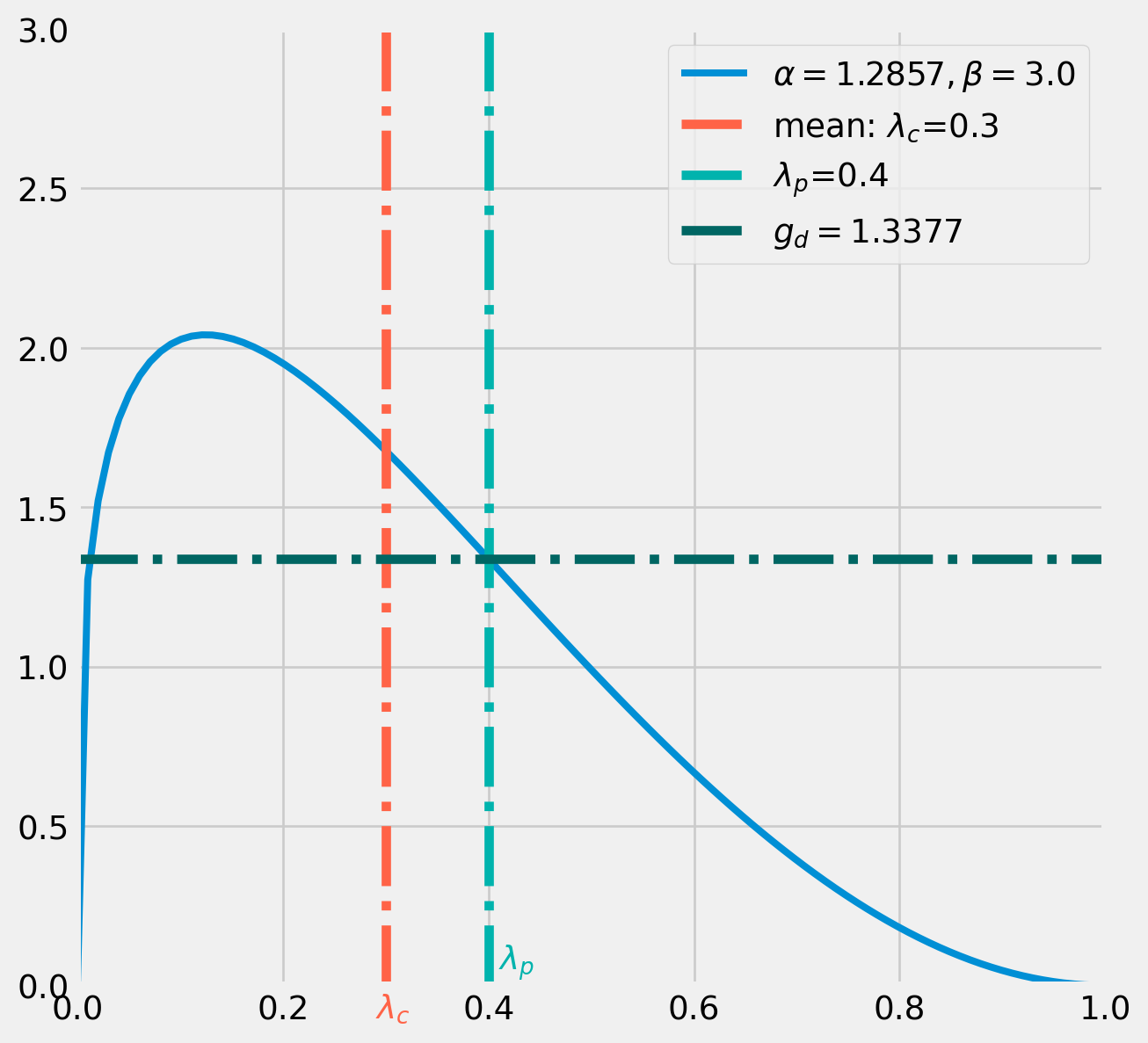

Suppose the initial value \(\lambda_{c} = .3\), the proposal distribution will be centered on \(.3\), however beta distribution has two parameters \(\alpha\) and \(\beta\), in order to pin down a unique combination of parameters for proposal distribution, one parameter needs to be assumed fixed as a tuning parameter.

Here we set \(\beta=3\) as our tuning parameter. According to the formula of mean \[ \mathrm{E}[X]=\frac{\alpha}{\alpha+\beta}=.3=\frac{\alpha}{\alpha+3} \] We pin down \(\alpha=1.2857\).

lamda_c = 0.3

lamda_p = 0.4

beta = 3

alpha = 0.9 / 0.7Next we draw from this proposal distribution, say we got \(\lambda_p = .4\).

With \[ \lambda_{c} = .3\\ \lambda_{p} = .4 \] Next we calculate the correction factor.

The denominator of correction factor \(g(\lambda_{p} = .4|\ \lambda_{c} = .3)\) means the probability of \(\lambda_{p} = .4\) from a beta distribution whose mean is \(\lambda_{c} = .3\).

g_d = sp.stats.beta.pdf(x=lamda_p, a=alpha, b=beta)x = np.linspace(0, 1, 100)

beta_pdf = sp.stats.beta.pdf(x, alpha, beta)

fig, ax = plt.subplots(figsize=(7, 7))

ax.plot(x, beta_pdf, lw=3, label=r"$\alpha = %.4f, \beta = %.1f$" % (alpha, beta))

ax.axvline(

lamda_c, color="tomato", ls="-.", label="mean: $\lambda_c$={}".format(lamda_c)

)

ax.text(0.29, -0.1, "$\lambda_c$", color="tomato")

ax.axvline(lamda_p, color="#00B3AD", ls="-.", label="$\lambda_p$={}".format(lamda_p))

ax.axhline(g_d, color="#006663", ls="-.", label=r"$g_d={:.4f}$".format(g_d))

ax.text(0.41, 0.05, "$\lambda_p$", color="#00B3AD")

ax.legend()

ax.axis([0, 1, 0, 3])

plt.show()<>:7: SyntaxWarning:

invalid escape sequence '\l'

<>:9: SyntaxWarning:

invalid escape sequence '\l'

<>:11: SyntaxWarning:

invalid escape sequence '\l'

<>:13: SyntaxWarning:

invalid escape sequence '\l'

<>:7: SyntaxWarning:

invalid escape sequence '\l'

<>:9: SyntaxWarning:

invalid escape sequence '\l'

<>:11: SyntaxWarning:

invalid escape sequence '\l'

<>:13: SyntaxWarning:

invalid escape sequence '\l'

/tmp/ipykernel_3474/1976243381.py:7: SyntaxWarning:

invalid escape sequence '\l'

/tmp/ipykernel_3474/1976243381.py:9: SyntaxWarning:

invalid escape sequence '\l'

/tmp/ipykernel_3474/1976243381.py:11: SyntaxWarning:

invalid escape sequence '\l'

/tmp/ipykernel_3474/1976243381.py:13: SyntaxWarning:

invalid escape sequence '\l'

\[ \frac{g(\lambda_{c}|\lambda_{p})}{g(\lambda_{p}|\lambda_{c})} \]

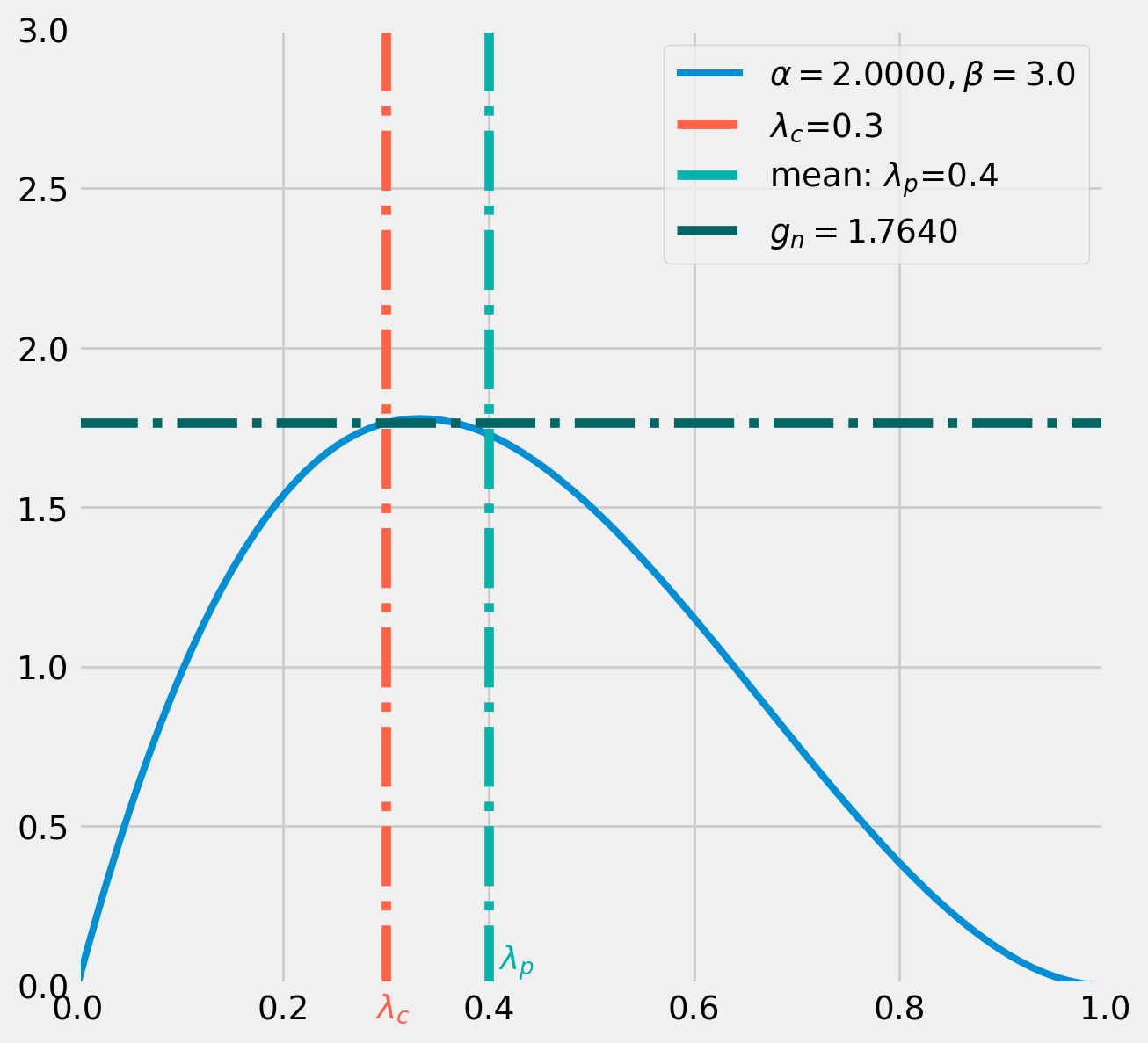

The numerator of correction factor \(g(\lambda_{c} = .3|\ \lambda_{p} = .4)\) means the probability of \(\lambda_{c} = .3\) from a beta distribution whose mean is \(\lambda_{p} = .4\).

Again use the formula \[ \mathrm{E}[X]=\frac{\alpha}{\alpha+\beta}=.4=\frac{\alpha}{\alpha+3} \] We pin down \(\alpha=2\).

beta = 3

alpha = 1.2 / 0.6

g_n = sp.stats.beta.pdf(x=lamda_c, a=alpha, b=beta)x = np.linspace(0, 1, 100)

beta_pdf = sp.stats.beta.pdf(x, alpha, beta)

fig, ax = plt.subplots(figsize=(7, 7))

ax.plot(x, beta_pdf, lw=3, label=r"$\alpha = %.4f, \beta = %.1f$" % (alpha, beta))

ax.axvline(lamda_c, color="tomato", ls="-.", label="$\lambda_c$={}".format(lamda_c))

ax.text(0.29, -0.1, "$\lambda_c$", color="tomato")

ax.axvline(

lamda_p, color="#00B3AD", ls="-.", label="mean: $\lambda_p$={}".format(lamda_p)

)

ax.axhline(g_n, color="#006663", ls="-.", label="$g_n={:.4f}$".format(g_n))

ax.text(0.41, 0.05, "$\lambda_p$", color="#00B3AD")

ax.legend()

ax.legend()

ax.axis([0, 1, 0, 3])

plt.show()<>:6: SyntaxWarning:

invalid escape sequence '\l'

<>:7: SyntaxWarning:

invalid escape sequence '\l'

<>:10: SyntaxWarning:

invalid escape sequence '\l'

<>:13: SyntaxWarning:

invalid escape sequence '\l'

<>:6: SyntaxWarning:

invalid escape sequence '\l'

<>:7: SyntaxWarning:

invalid escape sequence '\l'

<>:10: SyntaxWarning:

invalid escape sequence '\l'

<>:13: SyntaxWarning:

invalid escape sequence '\l'

/tmp/ipykernel_3474/1899102813.py:6: SyntaxWarning:

invalid escape sequence '\l'

/tmp/ipykernel_3474/1899102813.py:7: SyntaxWarning:

invalid escape sequence '\l'

/tmp/ipykernel_3474/1899102813.py:10: SyntaxWarning:

invalid escape sequence '\l'

/tmp/ipykernel_3474/1899102813.py:13: SyntaxWarning:

invalid escape sequence '\l'

Where \[ \frac{g_n}{g_d} = \frac{g(\lambda_{c}|\lambda_{p})}{g(\lambda_{p}|\lambda_{c})} \]

The correction factor finally equals

cf = g_n / g_d

cf1.3186423298548517MH Algorithm in Loop

Building the likelihood function \[ \mathcal{L}(k ; n, p)=\left(\begin{array}{l} n \\ k \end{array}\right) p^{k}(1-p)^{(n-k)} \]

def binom_lh(n, k, lamda):

lh = sp.special.binom(n, k) * lamda**k * (1 - lamda) ** (n - k)

return lhBuilding prior of beta distribution \[ f(x ; \alpha, \beta)=\frac{1}{B(\alpha, \beta)} x^{\alpha-1}(1-x)^{\beta-1} \]

def beta_prior(alpha, beta, lamda):

prior = (

(1 / sp.special.beta(alpha, beta))

* lamda ** (alpha - 1)

* (1 - lamda) ** (beta - 1)

)

return priorHere’s the full example Metropolis-Hastings algorithm.

def beta_binom_mh(

lamda_init=0.6,

n=10,

k=3,

alpha_prparams=0.5,

beta_prparams=0.5,

tuning_beta=3,

chain_size=10000,

):

np.random.seed(123)

lamda_current = lamda_init

lamda_mcmc = []

pass_rate = []

post_ratio_list = []

for i in range(chain_size):

# prior specification

log_lh_current = np.log(binom_lh(n=n, k=k, lamda=lamda_current))

log_prior_current = np.log(

beta_prior(alpha=alpha_prparams, beta=beta_prparams, lamda=lamda_current)

)

log_posterior_current = log_lh_current + log_prior_current

# parameter specification for proposal distribution

tuning_alpha = (lamda_current * tuning_beta) / (1 - lamda_current)

lamda_proposal = sp.stats.beta(a=tuning_alpha, b=tuning_beta).rvs()

# proposal specification

log_lh_proposal = np.log(binom_lh(n=n, k=k, lamda=lamda_proposal))

log_prior_proposal = np.log(

beta_prior(alpha=alpha, beta=beta, lamda=lamda_proposal)

)

log_posterior_proposal = log_lh_proposal + log_prior_proposal

# posterior ratio

log_post_ratio = log_posterior_proposal - log_posterior_current

post_ratio = np.exp(log_post_ratio)

# Correction factor

cf_denominator = sp.stats.beta.pdf(

x=lamda_proposal, a=tuning_alpha, b=tuning_beta

)

cf_num_alpha = (lamda_proposal * tuning_beta) / (1 - lamda_proposal)

cf_numerator = sp.stats.beta.pdf(x=lamda_current, a=cf_num_alpha, b=tuning_beta)

cf = cf_numerator / cf_denominator

# acceptance rule

prob_proposal = np.min([post_ratio * cf, 1])

unif_draw = sp.stats.uniform.rvs()

post_ratio_list.append(post_ratio)

if unif_draw < prob_proposal:

lamda_current = lamda_proposal

lamda_mcmc.append(lamda_current)

pass_rate.append("Y")

else:

lamda_mcmc.append(lamda_current)

pass_rate.append("N")

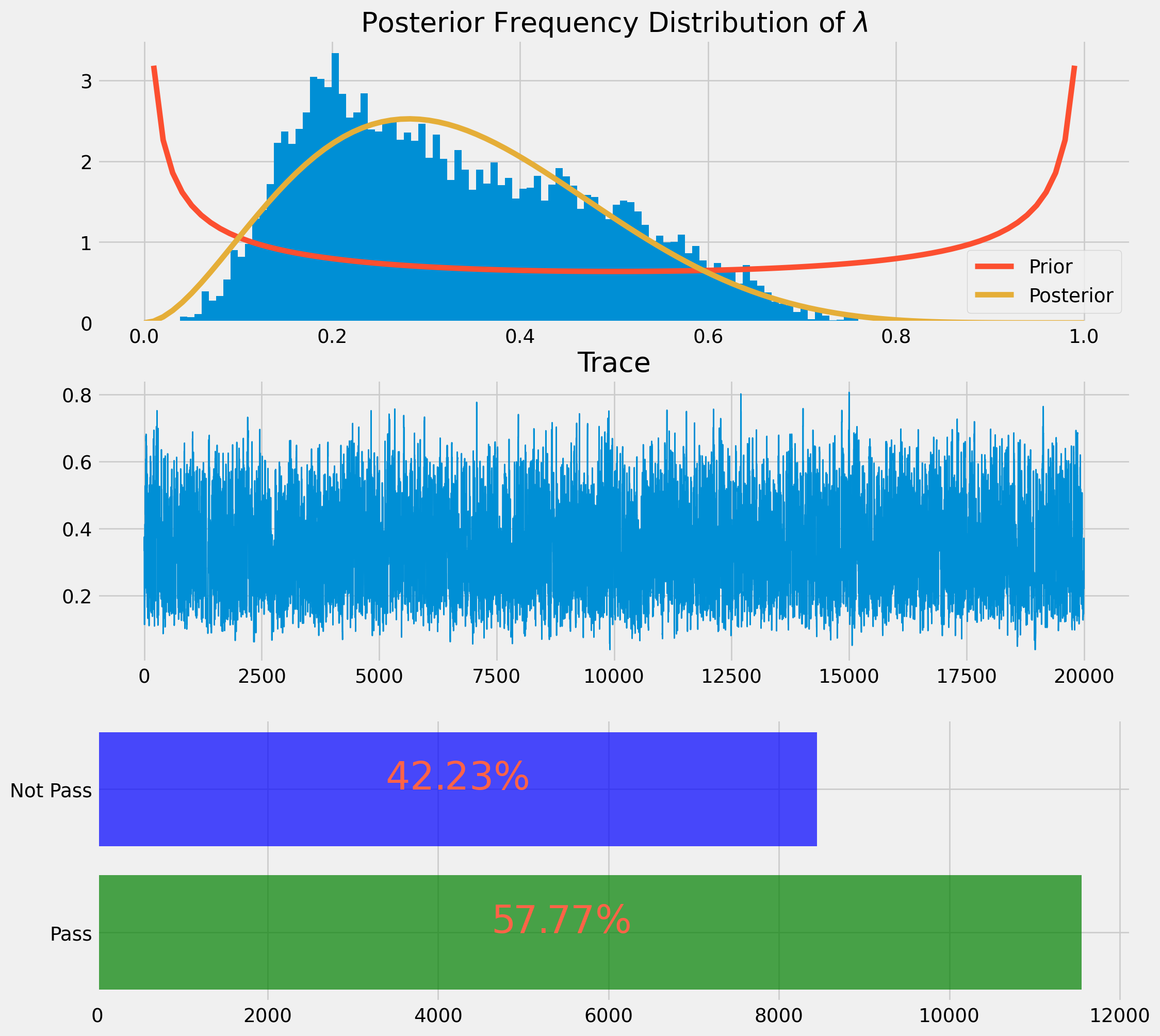

return lamda_mcmc, pass_ratelamda_mcmc, pass_rate = beta_binom_mh(n=10, k=3, tuning_beta=3, chain_size=20000)We will present the result as a histogram and a distribution plot. However this time the distribution plot will be obtained by moment matching rather than using analytical posterior form.

x = np.linspace(0, 1, 100)

alpha_pr, beta_pr = 0.5, 0.5

beta_pdf_prior = sp.stats.beta.pdf(x, a=alpha_pr, b=beta_pr)from scipy.optimize import fsolve

def solve_equ(x, mu=np.mean(lamda_mcmc), sigma=np.std(lamda_mcmc)):

a, b = x[0], x[1]

F = np.empty(2)

F[0] = a - mu * (a + b)

F[1] = a * b - (a + b) ** 2 * (a + b + 1) * sigma**2

return F

xGuess = np.array([6, 6])

z = fsolve(solve_equ, xGuess)alpha_post, beta_post = z[0], z[1]

print("alpha_post: {}".format(z[0]))

print("beta_post: {}".format(z[1]))

beta_pdf_post = sp.stats.beta.pdf(x, a=alpha_post, b=beta_post)alpha_post: 2.9118864790255863

beta_post: 5.869477871245038y_rate = pass_rate.count("Y") / len(pass_rate)

n_rate = pass_rate.count("N") / len(pass_rate)

yes = ["Pass", "Not Pass"]

counts = [pass_rate.count("Y"), pass_rate.count("N")]

fig, ax = plt.subplots(figsize=(12, 12), nrows=3, ncols=1)

ax[0].hist(lamda_mcmc, bins=100, density=True)

ax[0].set_title(r"Posterior Frequency Distribution of $\lambda$")

ax[0].plot(x, beta_pdf_prior, label="Prior")

ax[0].plot(x, beta_pdf_post, label="Posterior")

ax[0].legend()

ax[1].plot(np.arange(len(lamda_mcmc)), lamda_mcmc, lw=1)

ax[1].set_title("Trace")

ax[2].barh(yes, counts, color=["green", "blue"], alpha=0.7)

ax[2].text(

counts[1] * 0.4,

"Not Pass",

r"${}\%$".format(np.round(n_rate * 100, 2)),

color="tomato",

size=28,

)

ax[2].text(

counts[0] * 0.4,

"Pass",

r"${}\%$".format(np.round(y_rate * 100, 2)),

color="tomato",

size=28,

)

plt.show()

import numpy as np

def log_gaussian(x, mu, sigma):

# The np.sum() is for compatibility with sample_MH

return -0.5 * np.sum((x - mu) ** 2) / sigma**2 - np.log(

np.sqrt(2 * np.pi * sigma**2)

)

class BivariateNormal(object):

n_variates = 2

def __init__(self, mu1, mu2, sigma1, sigma2):

self.mu1, self.mu2 = mu1, mu2

self.sigma1, self.sigma2 = sigma1, sigma2

def log_p_x(self, x):

return log_gaussian(x, self.mu1, self.sigma1)

def log_p_y(self, x):

return log_gaussian(x, self.mu2, self.sigma2)

def log_prob(self, x):

cov_matrix = np.array([[self.sigma1**2, 0], [0, self.sigma2**2]])

inv_cov_matrix = np.linalg.inv(cov_matrix)

kernel = -0.5 * (x - self.mu1) @ inv_cov_matrix @ (x - self.mu2).T

normalization = np.log(

np.sqrt((2 * np.pi) ** self.n_variates * np.linalg.det(cov_matrix))

)

return kernel - normalization

bivariate_normal = BivariateNormal(mu1=0.0, mu2=0.0, sigma1=1.0, sigma2=0.15)